“Job Costing” to most users is more accurately described as – Is the job profitable? Most small “jobbing” type businesses more often than not rely upon “gut feel”.

Reckon Accounts includes excellent job costing functionality. The concept, design and indeed underlying code were all developed by Intuit within the QuickBooks product. The system is intuitive, comprehensive, easy to use, efficient and accurate.

Job Revenue

Less:

Labour Costs

Material Costs

Equals Job Profitability

Job Structure

Job Profitability Reporting

Limitations

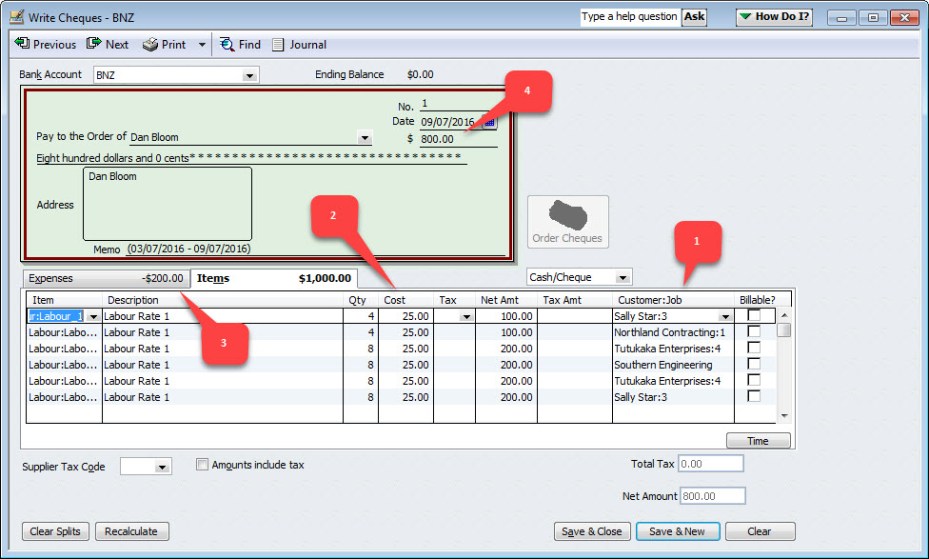

Job Revenue

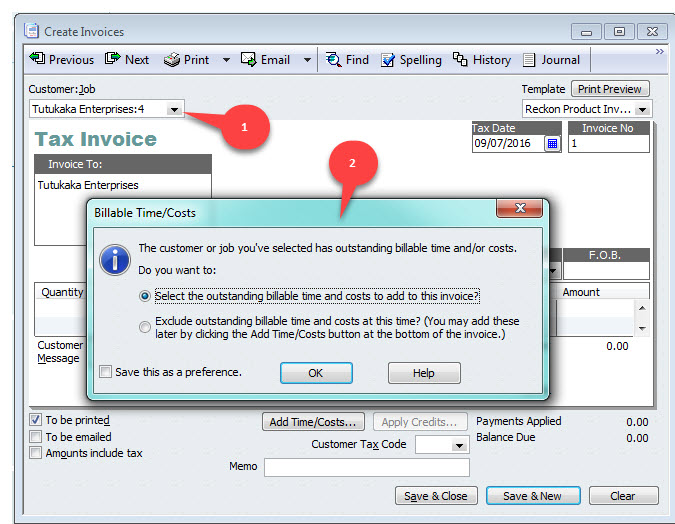

When the invoice process is initiated,

- The Customer/Job code is entered or selected.

- A dialogue is fired immediately to remind the user that the job has un-billed time and/or costs

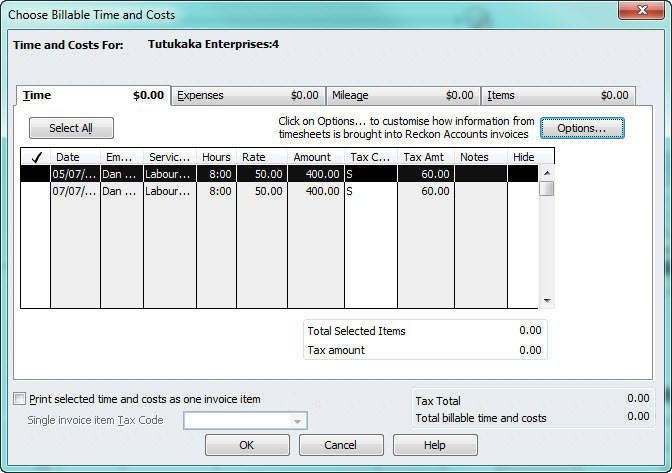

Selecting items, including time charges, expenses, mileage and/or items allocated to the job will transfer the costs to the invoicing display. Once the items have been transferred to the invoice, they can be manipulated by changing descriptions, selling prices, quantities, etc. This approach is typically very efficient for ‘charge-up’ jobs where time and materials are being invoiced.

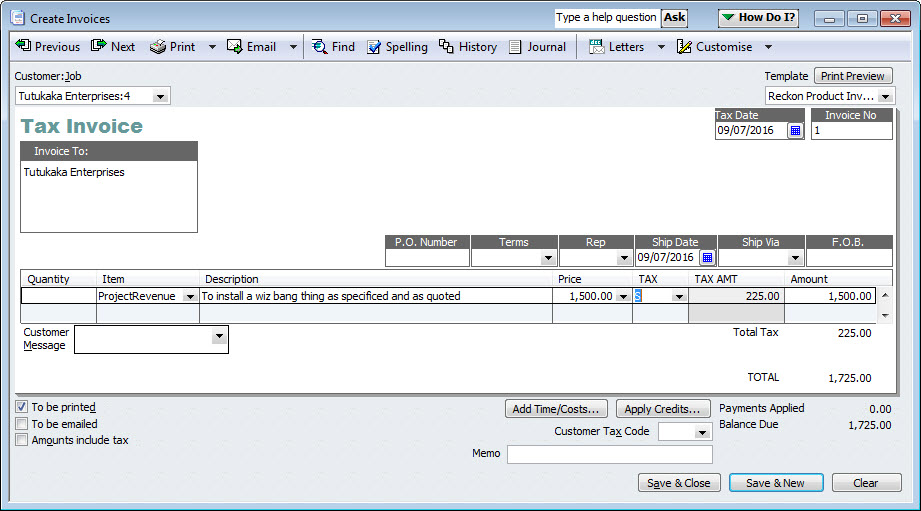

Alternatively, fixed or agreed pricing can simply be invoiced for the job

Labour Costs

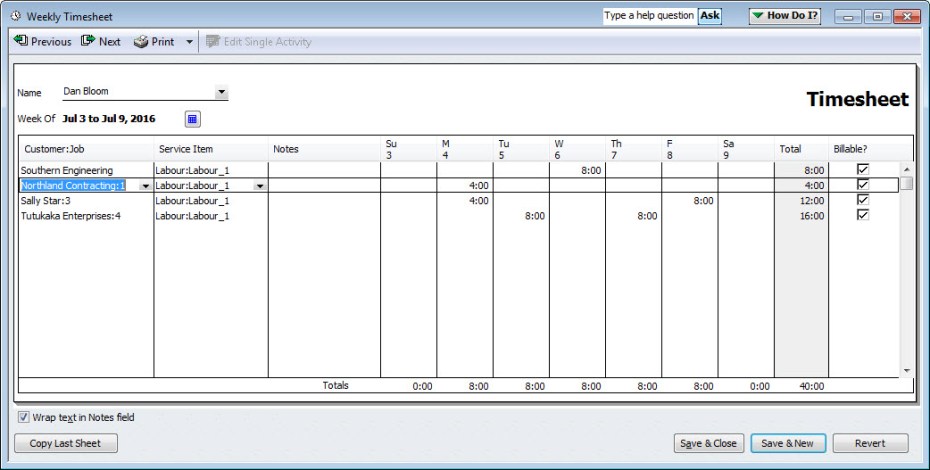

Time Charges are easily captured within Reckon via a Timesheet. Efficiency is enhanced when we front end the accounting system with an electronic time capture system such as TSheets. Time capture via TSheets will update the Reckon TimeSheet.

Time accumulated on the time sheet will become available within the accounting system to supply data to the onboard Payroll Systems, Invoicing – to be charged to the customer and payment processing.

Labour Costs entered on the time sheet will automatically populate the job records when the employee is paid. The payment process can be via the onboard payroll system or recorded as a standard payment transaction within the accounting system. The recording of the payment will:

- Identify the customer/job code – originally sourced form the time sheet

- Typically use the employee’s actual gross pay rate

- Allow for deductions such as PAYE

- Record the net amount the employee was actually paid

Material Costs

As expenses are incurred, each financial transaction will have the option to ‘tag’ the costs to a specific job.

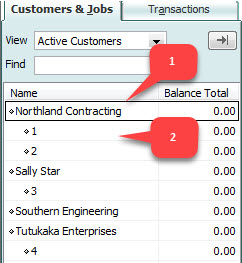

Job Structure

Easy to define – easy to use – exceptionally well organised. Jobs can be created within a hierarchy – including multiple levels. In most cases, the structure is created with the (1) customer as the ‘parent’ or highest level, with (2) jobs clearly defined under the parent. Any naming/number convention can be used for both ‘parent’ account and the underlying jobs.

Most other small business accounting systems cannot match this simple and effective structure.

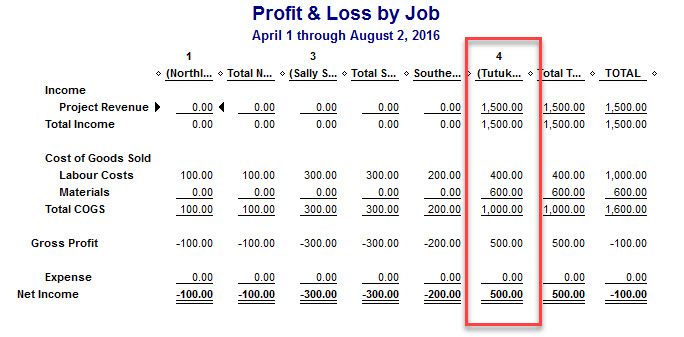

Job Profitability Reporting

Reckon via the legacy QuickBooks design offers excellent job profitability reporting including very useful user control of filters and formating to ensure the reporting is suitable to alternative requirements.

Limitations

Accuracy is however limited by 3 major factors. Remember – Job Costing is occurring within a rigid accounting system – thus rigid, accounting rules are being applied to every transaction recorded within the system – Each of the limitations are driven by fundamental accounting rules.

The first limitation is the user. Sorry, yes it might well be your fault. A good foundation in accounting concepts and/or vigilant/consistent compliance to procedures is required to ensure accurate costing results.

The second limitation relates to the use of ‘real money’ – instead of ‘funny money’. Best we explain that one – When you pay staff say $20 per hour is that the cost which should be posted to a job. Most will argue no – not at all. The $20/hour rate is diluted with part of it going the the tax man. Significantly more distortion is caused by other costs & overheads always incurred to have that member of staff on-board. The real cost of the employee is more likely to be $30/hour. The Reckon/QuickBooks design makes it easy to record the $20/hour, but rather difficult to record the $30/hour.

The third limitation is caused again by the real money concept. Reckon/QuickBooks looks for the actual spend (accrued or cash) to trigger the financial recording. You cannot move stocked items to a job easily nor is recorded time charged to the job. You must complete the transaction cycle in most cases to ensure the completion of the job cost postings.